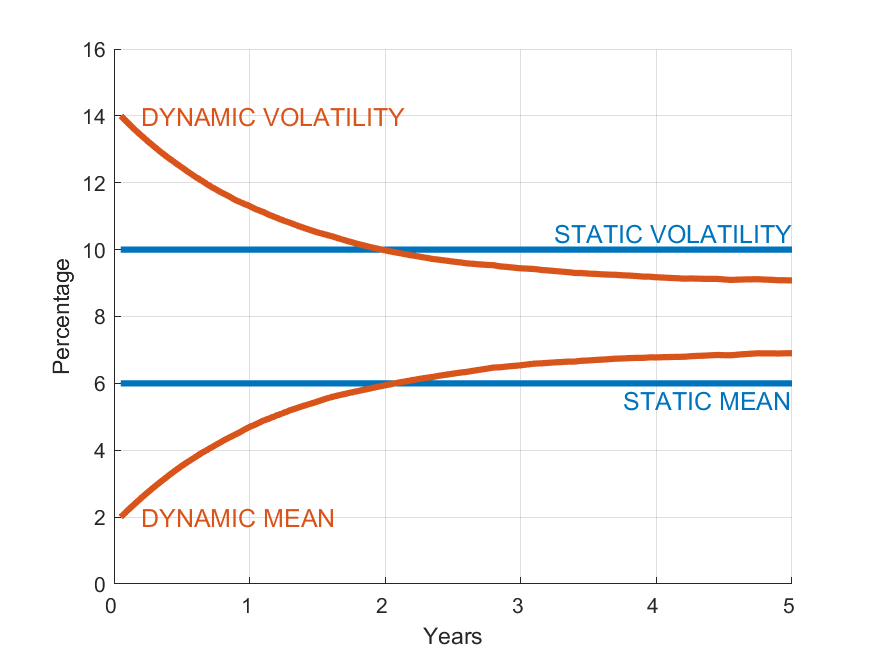

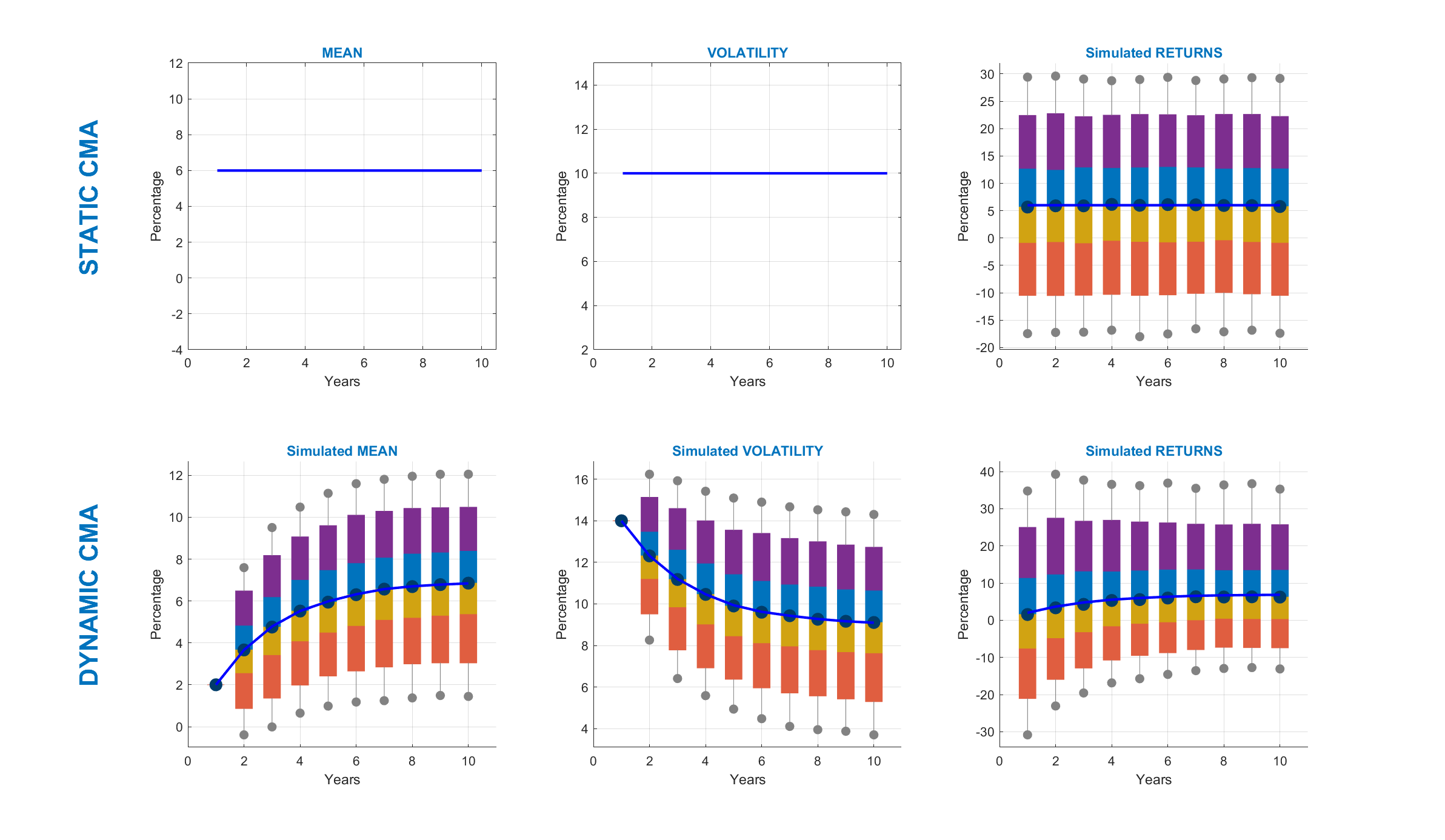

Dynamic Mean and Volatility assumptions are stochastic in nature and can be simulated using typically mean-reverting processes based on:

Long-term target levels for Mean and Volatility.

Speed of mean-reversion for Mean and Volatility.

Volatility assumptions for Mean and Volatility.